Why Was My Roof Insurance Claim Denied? (5 Common Reasons + What To Do Next)

Published on May 5, 2026

You filed a claim after a storm, expecting your insurance to help cover the damage.

Then the decision comes back, and it is not what you expected. Your roof insurance claim was denied.

Now you’re left trying to figure out what happened. You may still see damage. You may even have leaks or concerns about your roof’s condition. But the insurance company is saying your roof does not qualify.

You start asking yourself:

Why was my roof insurance claim denied?

Is the insurance company right?

Was something missed during the inspection?

What should I do next?

A denied claim does not always tell the full story. It tells you how the insurance company interpreted the situation, not necessarily what your roof actually needs.

At KangaRoof, we have worked with thousands of homeowners on their roof insurance claims and have seen many reasons why a claim has been denied. We’ve helped thousands of homeowners understand why they were denied, whether they should resubmit their claim, and documents to include when resubmitting to get approved.

From this article, you will learn the most common reasons claims get denied, how to review that decision, and what your next step should be based on real information.

Why would a roof insurance claim be denied?

A roof insurance claim is usually denied because the insurance company believes the damage is not covered under the policy, does not meet the policy requirements, or was not caused by a covered event.

That sounds simple, but the reasons behind a denial can vary widely.

Some of the most common reasons include:

- The damage is being labeled as wear and tear, not storm damage

- The roof is old, and the insurer believes the condition is age-related

- The damage is considered minor and below your deductible

- The claim was filed too late

- The insurer says the damage existed before the storm

- Poor maintenance is being blamed for the issue

- There is not enough documentation to support the claim

- The policy has exclusions that limit roof coverage

In many cases, the denial comes down to one core issue. The insurance company does not believe the roof damage qualifies for coverage under the policy.

That is why the next step should never be panic. It should be understood exactly why the claim was denied.

Does a denied claim mean there is no roof damage?

No. A denied claim does not automatically mean your roof is fine.

It means the insurance company has decided not to pay based on how they interpreted the cause, condition, or severity of the damage.

That is an important distinction.

A roof can still have real problems even if the claim is denied. You may have:

- Damaged shingles

- Lifted or creased tabs

- Granule loss after hail

- Leaks caused by compromised flashing

- Soft spots or decking issues

- Gutter or vent damage that points to a larger problem

The real question is not just whether damage exists. The real question is whether the insurer believes that damage is covered.

This is where homeowners can get stuck. They hear “denied” and assume there is no issue, or they assume the carrier must be right. But insurance decisions and roof condition are not always the same thing.

A denied claim should lead to a second look, not an automatic conclusion.

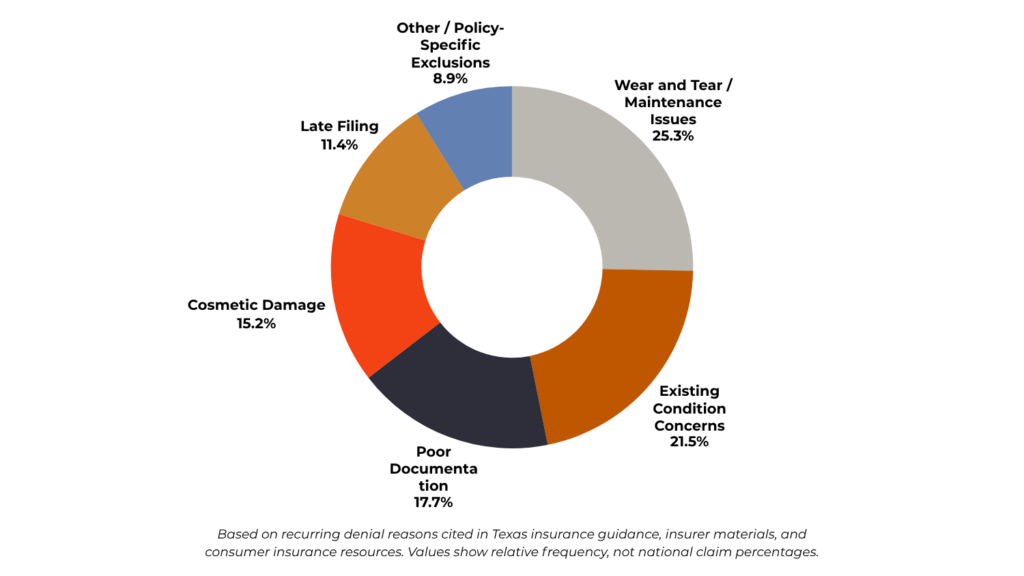

What are the most common reasons roof claims get denied in Texas?

In Austin and throughout Central Texas, denied roof claims often stem from a few recurring issues.

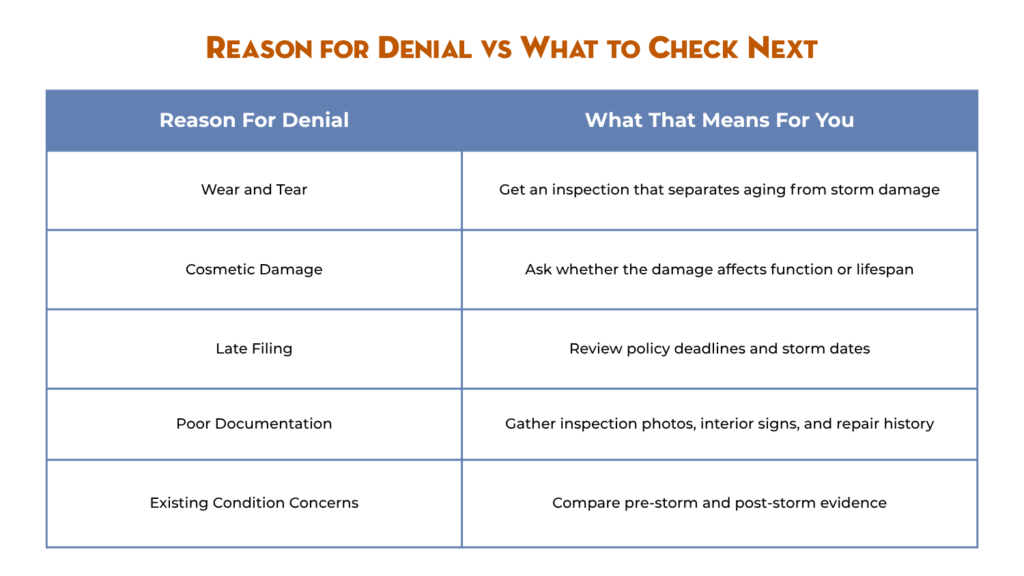

The insurer says it is wear and tear

This is one of the most common reasons for denial.

Insurance is designed to cover sudden, accidental damage from a covered event. It is not meant to pay for an older roof that has simply reached the end of its life.

If the adjuster believes the condition resulted from age, long-term exposure, poor maintenance, or prior deterioration, the claim may be denied.

The damage looks cosmetic, not functional

The carrier may agree that hail or wind hit the roof, but still argue that the impact did not create functional damage.

For example, they may say:

- The shingles were marked but still sealed properly

- The metal components were dented but still work

- The roof has signs of weathering, but not enough damage to justify replacement

The roof is already in poor condition

If the roof had existing issues before the storm, that can complicate the claim.

The insurer may argue that:

- The storm did not cause the main problem

- The roof was already failing

- Prior repairs, patchwork, or neglected areas affected performance

The claim was reported too late

Waiting too long can make it harder to prove the claim.

If months pass before the damage is reported, the insurer may argue that:

- New weather events could have changed the roof

- The damage cannot be tied clearly to one storm

- The homeowner did not act quickly enough to prevent further damage

The documentation was weak

Photos from the ground, incomplete notes, or insufficient inspection detail can hurt a claim.

When the evidence is thin, the carrier may decide there is not enough support for coverage.

How do you know if the insurance company got it wrong?

You will not know just by looking at the denial letter alone.

The best way to evaluate the decision is to compare three things:

- What the insurance company said

- What the roof is actually doing

- What a qualified roofing professional sees during inspection

Start by reading the denial letter carefully.

Look for the specific reason given. Not the general tone. Not the summary. The actual stated reason.

Then compare that with the roof’s condition.

Ask questions like:

- Is there visible storm-related damage?

- Are there leaks or signs of water intrusion?

- Are metal components, vents, soft metals, or gutters showing impact?

- Does the pattern of damage match a recent storm event?

- Does the roof show isolated storm damage or broad age-related decline?

A good inspection can help separate opinion from evidence.

That matters because some denials are valid. Others are incomplete, rushed, or based on limited information. You need facts before deciding which one you are dealing with.

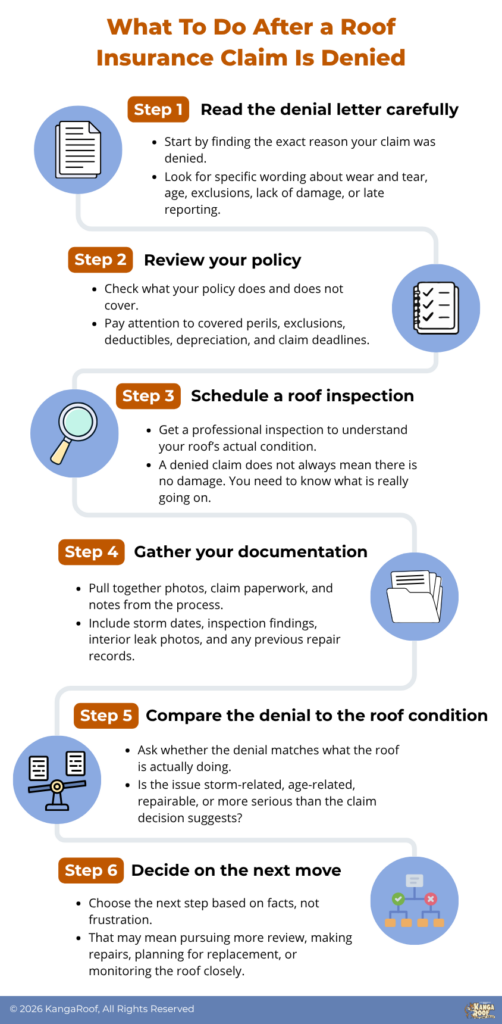

What should you do first after a roof insurance claim is denied?

The first step is to slow down and get organized.

You have options. Do not sign a large repair contract out of frustration. And do not ignore the roof and hope it holds.

Start here:

Find the exact reason the claim was denied.

You want to know whether the insurer is saying:

1. Read the denial letter closely

- The damage is excluded

- The damage is not severe enough

- The cause of loss is not covered

- The roof condition is pre-existing

2. Review your policy

You do not need to become an insurance expert overnight.

But you should review the parts that affect your roof claim, including:

- Covered perils

- Exclusions

- Deductible

- Depreciation language

- Filing deadlines

- Repair or replacement terms

3. Get a roof inspection from a trusted contractor

You need an independent evaluation of the roof condition.

A thorough inspection should help answer:

- Is there storm damage?

- Is the roof repairable?

- Is the damage localized or widespread?

- Does the condition look age-related, maintenance-related, or event-related?

- Are there related exterior items damaged, too?

4. Document everything

Gather:

- Photos of the roof and exterior

- Interior leak photos, if applicable

- The denial letter

- Claim paperwork

- Notes from conversations with the adjuster

- Dates of recent storms, if known

- Any previous repair records

5. Ask whether the denial should be challenged

Not every denial should be pushed. But some should be reviewed more closely.

The next step depends on the strength of the evidence. Often, you have the right to request a reinspection by a different adjuster.

Can you appeal or reopen a denied roof claim?

Sometimes, yes.

If new evidence comes to light or the denial appears to be based on incomplete information, the claim may be worth revisiting.

That does not mean every denial will be reversed. But it does mean a denial is not always the final word.

Situations where further review may make sense include:

- The roof inspection shows storm damage that was missed

- The adjuster only inspected limited areas

- Important documentation was not included the first time

- The cause of damage may have been misclassified

- Interior and exterior evidence together tell a different story

A contractor can help document roof conditions and explain what they are seeing. That can give you clearer support if you decide to ask the carrier for another review.

What matters most is whether the evidence supports a covered loss.

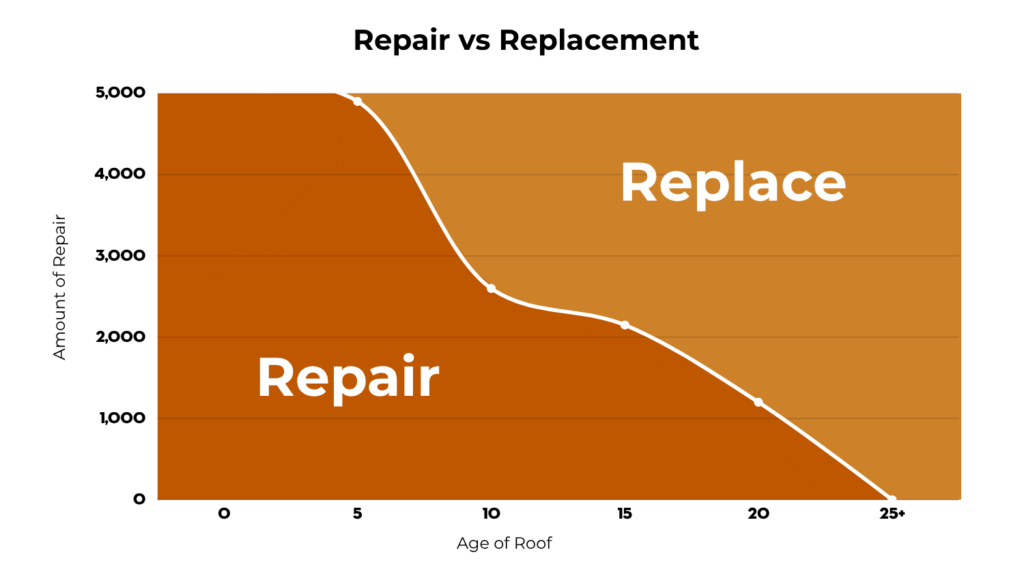

Should you repair the roof even if insurance will not pay?

Sometimes, yes.

If the roof has a real problem, delaying repairs can lead to higher costs later.

A denied claim does not stop leaks. It does not prevent decking damage. It does not protect insulation, ceilings, framing, or interior finishes.

If the damage is minor, a repair may be the best next step.

If the roof is older and the problem is widespread, replacement may still be the better long-term decision, even without insurance funds.

This is where homeowners need clarity, not pressure.

You want to know:

- What needs attention now

- What can wait

- What a repair will actually solve

- Whether the repair money would be better put toward a replacement

- How much more life does the roof likely have

What if the denial is really about roof age?

Older roofs often create gray areas in insurance claims. The insurer may say the storm did not cause the failure, while the homeowner sees a roof that clearly needs help.

In that case, focus on the decision in front of you:

- Can repairs reasonably extend its life?

- Is a replacement the more practical investment?

- Will waiting increase the risk of interior damage or emergency costs?

This is where a homeowner needs straight answers.

Not every older roof should be replaced right away. But not every older roof is worth patching either.

The goal is to understand the roof’s actual condition and make the best next decision from there.

How can a roofing contractor help after a denied claim?

A good roofing contractor should help you understand the roof, not just sell a job.

That means helping you answer practical questions like:

- Is there real storm damage here?

- Is the denial consistent with the roof condition?

- Is repair possible?

- What happens if I wait?

- What will this likely cost if insurance does not cover it?

A contractor can also help by:

- Documenting visible damage clearly

- Explaining what appears storm-related versus age-related

- Showing whether problems are isolated or widespread

- Identifying urgent repairs that protect the home now

- Giving you a realistic repair or replacement path

What they should not do is create more confusion.

If you are already frustrated by a denied claim, the last thing you need is vague language or high-pressure sales talk. You need a clear explanation of what the roof is doing and what options actually make sense.

The bottom line on a denied roof insurance claim

A denied roof insurance claim can leave you feeling stuck, but it should not leave you guessing.

The next step depends on why the claim was denied and on the condition of your roof. In some cases, the denial is correct, and the issue is age or maintenance. In other cases, the roof deserves a closer look before you decide what to do next.

The goal is not to force a claim to work. The goal is to understand the facts, protect your home, and make the smartest decision from here.

Need help understanding what to do next?

If your roof insurance claim was denied and you are unsure whether the decision makes sense, start with a thorough inspection.

At KangaRoof, we’ve helped thousands of Central Texas homeowners understand what is happening on their roof, what the damage may mean, and whether repair or replacement makes the most sense.

If you want straightforward answers without pressure, schedule an inspection and get clarity on your next step.