Key Takeaways

- An insurance supplement is a request submitted to the insurance company for additional funds when damage or required repairs are discovered that were not included in the original insurance estimate.

- Supplements are common in roof insurance claims.

- Building code requirements, hidden damage, and missing scope items are frequent reasons supplements occur.

- A supplement does not increase your deductible.

- Legitimate supplements are not insurance fraud.

If you're going through a roof insurance claim, you may hear your contractor mention filing a supplement with your insurance company.

That's when homeowners often start asking important questions about their claim.

If the insurance company has already inspected the roof and approved the claim,

Why is a supplement needed?

Does it increase your deductible?

Is it normal for contractors to ask for additional funds after the claim has already been approved?

At KangaRoof, we hear these questions every day from homeowners across Austin and Central Texas. The reality is that supplements are one of the most misunderstood parts of the insurance claims process, despite being incredibly common.

In this article, you'll learn exactly what a supplement is, why supplements happen, when they're appropriate, and how they can help ensure your roof is restored properly after storm damage. By the end, you'll understand what role supplements play in an insurance claim and what to expect if one becomes necessary on your project.

What Is a Supplement?

A supplement is a request for additional insurance funds when work, materials, or damage were not included in the original insurance estimate.

In simple terms, it is a correction or update to the insurance scope of work.

Supplements are common in property insurance claims because insurance adjusters often inspect dozens of properties each week and must create estimates based on what is visible at the time of inspection.

Once a roofing contractor begins preparing for the project, they may discover:

- Missing line items

- Code-required upgrades

- Additional storm damage

- Incorrect material quantities

- Labor costs that were not included

- Components that cannot be reused

- Damage that cannot be seen until work begins

When this happens, documentation is submitted to the insurance carrier for review.

If approved, the carrier issues additional funds to cover the necessary work.

Why Do Supplements Happen?

Supplements happen because roofing projects often reveal information that was not available during the initial inspection.

Insurance adjusters typically inspect roofs from the exterior. They may not have access to every detail needed to build a complete restoration scope.

Some common reasons for supplements include:

Building Code Requirements

Local building codes may require upgrades that were not included in the original estimate.

Examples include:

- Additional underlayment requirements

- Ventilation improvements

- Ice and water barrier requirements in certain situations

- Flashing replacement requirements

Material Availability

The original roofing materials may no longer be available.

If matching materials cannot be sourced, the scope may need to be adjusted.

Hidden Damage

Additional damage sometimes becomes visible after materials are removed.

Examples include:

- Damaged decking

- Rotten wood

- Water intrusion

- Structural concerns

Missing Scope Items

Insurance estimates occasionally omit necessary components such as:

- Starter shingles

- Ridge caps

- Drip edge

- Flashing

- Ventilation components

- Detachment and reset items

A supplement helps ensure these items are considered.

Does a Supplement Increase My Deductible?

No.

A supplement does not increase your deductible.

Your deductible remains the same regardless of whether the insurance company approves additional funds.

In most cases, a supplement simply helps ensure the insurance carrier pays for work that should have been included from the beginning.

If your deductible is $2,500, it remains $2,500 whether the claim settles at $15,000 or $25,000.

Is Filing a Supplement Insurance Fraud?

No, not when it is legitimate and properly documented.

A valid supplement is a normal part of the insurance restoration process.

Insurance carriers expect supplements and review them every day.

The key is documentation.

A reputable contractor should provide:

- Photos

- Measurements

- Manufacturer requirements

- Building code references

- Material documentation

- Detailed explanations of the requested items

The goal is not to inflate the claim.

The goal is to ensure the scope accurately reflects the work required to restore the property.

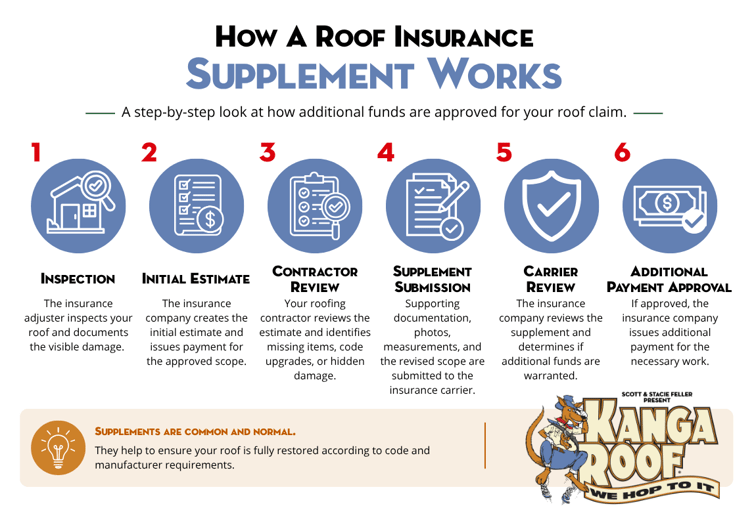

Who Files the Supplement?

In most cases, the contractor submits the supplement package.

The process usually looks like this:

- The insurance company creates the initial estimate.

- Contractor reviews the estimate.

- Missing items or discrepancies are identified.

- Supporting documentation is collected.

- Supplement request is submitted.

- The insurance company reviews the request.

- Additional funds are approved or adjusted.

The homeowner typically does not need to prepare the documentation themselves.

However, homeowners should stay informed throughout the process and ask questions if they do not understand what is being submitted.

How Long Does the Supplement Process Take?

The timeline varies by insurance company and claim complexity.

Simple supplement requests may be reviewed within a few days.

More complex requests can take several weeks.

Factors that affect timing include:

- Carrier response times

- Storm volume in the area

- Size of the claim

- Documentation quality

- Whether additional inspections are needed

The better the documentation, the faster the process often moves.

Should Homeowners Be Concerned About Supplements?

Not necessarily.

A supplement is not automatically a red flag.

In fact, it may indicate that your contractor is carefully reviewing the scope to ensure nothing important gets overlooked.

What matters is transparency.

Ask your contractor:

- What items are being supplemented?

- Why were they not included originally?

- What documentation supports the request?

- How does it affect the project timeline?

A good contractor should be able to explain every item clearly.

What Happens If the Insurance Company Denies the Supplement?

Insurance companies do not approve every supplement request.

If a request is denied, several outcomes are possible:

- Additional documentation may be submitted.

- The carrier may partially approve the request.

- The contractor and carrier may discuss the scope further.

- The homeowner may choose whether to proceed with optional work not covered by insurance.

The important thing to remember is that supplements are requests, not guarantees.

Approval depends on the facts, documentation, policy language, and claim circumstances.

What Homeowners Need to Remember About Supplements

A supplement is a tool used to ensure an insurance claim accurately reflects the work required to restore your roof.

It does not mean someone made a mistake. It does not mean anyone is trying to inflate the claim.

In many cases, it is a normal part of the process.

The most important thing is understanding why the supplement is being submitted and ensuring the request is supported by proper documentation.

When handled correctly, supplements help homeowners receive the coverage they are entitled to under their policy and help ensure the roof is restored properly.

Want a Second Set of Eyes on Your Claim?

You don't have to navigate the insurance process alone.

If you're wondering whether your estimate is accurate, whether a supplement is justified, or what happens next, KangaRoof can help you understand your options without pressure or obligation.

Schedule a free inspection and claim consultation today.

{kind=link}